Stacie Hernandez+FollowWhen $350K a year isn’t enoughEarning $350,000 a year might sound like financial security, but for Nick and Lauren, it’s a tightrope walk. As their kids approach college and expenses pile up—think mortgage, car leases, and all those little extras—what once felt comfortable now feels stretched. Raises and bonuses just raise the bar for spending, not savings. The real challenge? Balancing college costs, retirement plans, and the lifestyle they’ve grown used to. It’s a wake-up call: high income doesn’t always mean peace of mind. How do you keep your family’s future on track when every dollar already has a job? #Business #PersonalFinance #FamilyBudget00Share

Joseph Livingston+FollowHow to Snag a Bigger IRS Refund in 2026Tax season hack: Want your refund faster and bigger? Skip the paper check and get direct deposit into a bank account—no more waiting or losing cash to check-cashing fees. Plus, if you make under $67k, check out free tax help at VITA sites. That’s more money in your pocket for bills, savings, or even a treat-yourself splurge. Don’t let fees eat your refund! #Business #MakeMoney #TaxRefund #MoneyHacks #IRS #PersonalFinance #TaxSeason10Share

Alexander Black+FollowWould You Buy a Car for Half Your Salary?Imagine leasing a car for three years, then being told you can buy it for $19K—even though you and your spouse only make $40K a year. Sounds like a steal, right? Not so fast. The Ramsey Show hosts say it’s a trap: most Americans are living paycheck to paycheck, and taking on more debt for a car is a fast track to broke. Their advice? Ditch the loan, consider going one-car, and don’t let a “deal” wreck your finances. #Cars #PersonalFinance #DebtFreeJourney00Share

Danielle Anderson+FollowWhy Japan's Bond Drama Could Hit Your WalletHeads up: Japan's bond market just threw a fit over government spending, and Ken Griffin says the US could be next. If investors start worrying about America’s debt, we could see higher mortgage rates and pricier loans. It’s like when your credit card bill gets too high—suddenly, everything costs more. So, keep an eye on those headlines; what happens in Japan might just show up in your monthly payments soon. #Business #Market #PersonalFinance00Share

Emily Rogers+FollowHow ignoring your IRA could cost you bigRolling over $50K from a 401(k) to a Traditional IRA seemed like a smart move—until five years later, the account had barely grown. While the stock market soared, this investor’s balance only ticked up $2K, likely eaten away by fees and ultra-conservative fund choices. Turns out, “set it and forget it” doesn’t mean never check in. Many in the personal finance community say it’s a wake-up call: even if you trust your advisor, you still need to keep tabs on your investments. Have you ever been surprised by your account’s performance? #Business #MakeMoney #PersonalFinance00Share

Aaron Ballard+FollowIs $1.4M Really the New 50s Net Worth?Heard the buzz that the average American in their 50s is now a millionaire? Here’s the catch: that $1.4 million average is pumped up by a few mega-rich folks. Most people in their 50s are doing well if they’ve got a paid-down house and some retirement savings, but they’re not rolling in cash. The real money hack? Start investing early, stick with it, and let time do the heavy lifting. Home equity and steady saving are the real MVPs, not lottery wins or flashy trades. #RealEstate #MoneyTalk #PersonalFinance10Share

laura54+FollowHow to Keep a Windfall Safe From OverspendingImagine getting a $1.2 million payout, but you’re worried your spouse might burn through it. That’s the real-life dilemma a young husband with months to live posted on Reddit. The crowd’s advice? Set up a trust to manage the money, so it pays out in steady monthly checks instead of one big lump sum. It’s like putting your inheritance on autopilot—no impulse shopping sprees, just long-term security. If you ever get a big payout, consider this move to protect your loved ones (and their wallets). #Business #MoneyLifehacks #PersonalFinance00Share

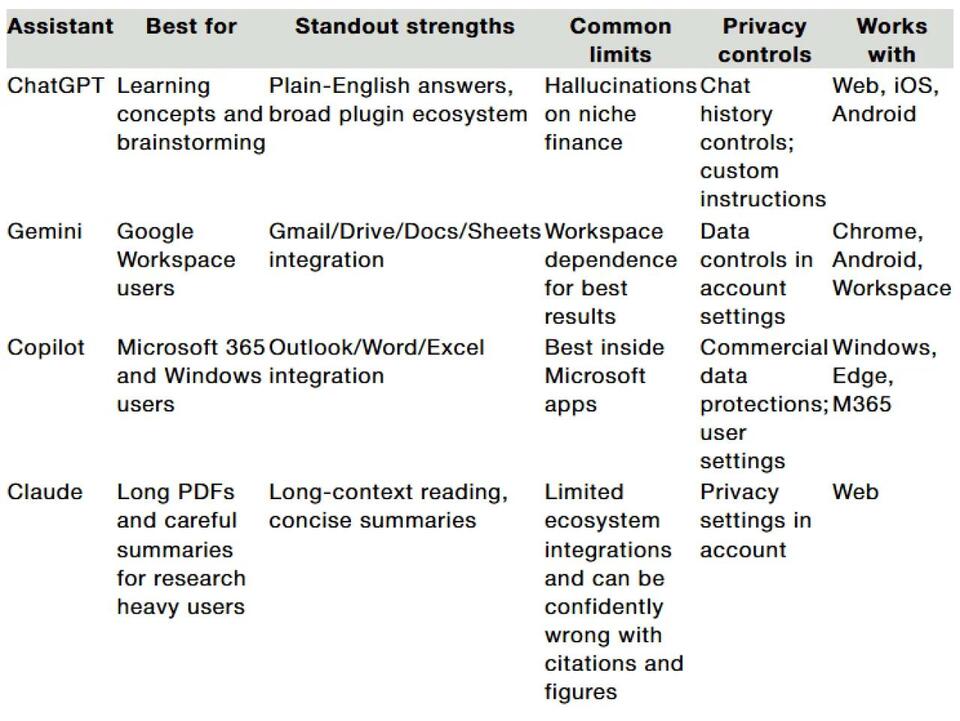

Kara Rosario+FollowWhich AI Assistant Wins at Money Management?Let’s talk about the real-world strengths and gaps of AI personal finance assistants. ChatGPT is a champ at breaking down financial concepts, while Gemini is a dream for Google power users. Copilot fits seamlessly with Microsoft tools, and Claude shines at digesting long documents. But here’s the kicker: none are perfect for personalized advice, and privacy is a real concern. Would you trust an AI with your budget, or is human expertise still king? #Tech #AI #PersonalFinance00Share

Linda Price+FollowCan Billionaires Bail Out America? Not Even CloseEver wondered if the richest folks in America could just pay off the national debt? Turns out, even if every billionaire sold everything and handed over their cash, it’d only cover a small slice of the $38 trillion tab. So, no superhero bailout here. The real fix? Smarter spending and growing the economy—think less about billionaire checks, more about everyone pitching in and boosting innovation. Next time you hear about the national debt, just remember: it’s not a one-person problem! #Business #MoneyTalks #PersonalFinance01Share

walkerjason+FollowCar Loans Are Getting Wildly LongCar loans are stretching out to 84 months (yep, 7 years!) and more people are signing up for $1,000+ monthly payments just to afford a new ride. But here’s the kicker: all that extra time means you could pay thousands more in interest—sometimes almost as much as the car itself! If you’re car shopping, double-check those loan terms before you sign. Your wallet will thank you later. #Cars #CarLoans #PersonalFinance31Share